VAT exemption thresholds vary widely across Europe, with Switzerland, the United Kingdom, and France having the highest nominal thresholds among 32 major European countries in 2026. These thresholds reduce compliance costs for small businesses but can also distort business behavior by encouraging firms to stay below the VAT registration cutoff.

Across the countries reviewed, Switzerland has the highest absolute VAT exemption threshold at CHF 100,000, equivalent to €106,724. The United Kingdom follows at £90,000, or €105,043, while France has a threshold of €87,000.

Spain and Turkey are the only countries in the group with no VAT exemption threshold, meaning all businesses are enrolled in the VAT system.

VAT thresholds adjusted for purchasing power

Nominal thresholds do not show the full economic impact because price levels differ across countries. When adjusted for purchasing power parity, Romania has the highest threshold at RON 395,000, equivalent to $202,206.

The next highest thresholds on a purchasing power basis are:

- Czech Republic: CZK 2,000,000, equivalent to $155,039

- Italy: €85,000, equivalent to $140,246

This means a threshold that appears lower in euro terms may still represent a larger economic exemption in countries with lower price levels.

Why VAT thresholds matter

VAT registration thresholds reduce administrative and compliance costs for small businesses. They allow smaller firms to avoid the complexity of collecting, reporting, and remitting VAT.

However, these thresholds also reduce tax revenue and create uneven treatment between small and larger firms. Businesses below the threshold receive a tax advantage, while firms above the threshold must comply with VAT rules.

This can discourage business growth. A high threshold may make it more attractive for firms to remain small instead of expanding and achieving economies of scale.

The VAT “tax cliff” problem

High VAT exemption thresholds create a “notch,” or tax cliff, at the registration cutoff.

A business that exceeds the threshold by even one euro may become liable for VAT on its entire value added, not just on the amount above the threshold. This creates a strong incentive to remain below the line.

Empirical work finds that firms respond by underreporting turnover or scaling back real activity to avoid crossing the threshold.

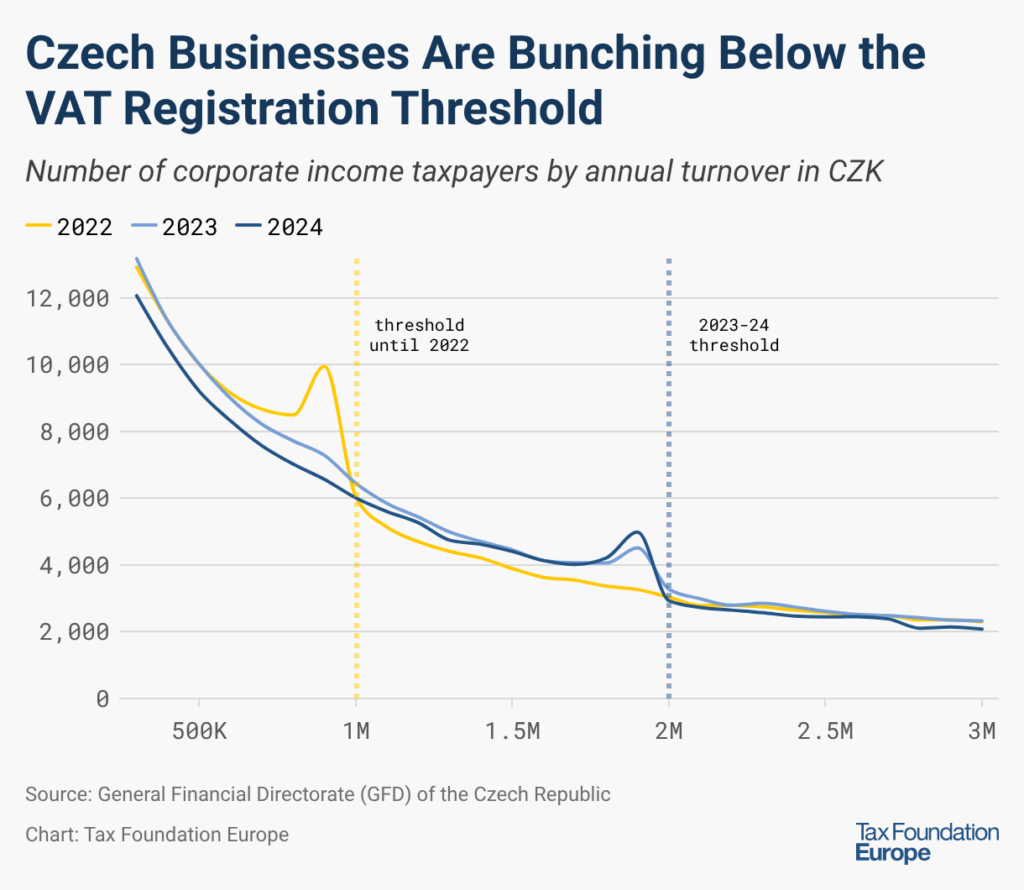

The Czech Republic illustrates this effect. It has one of the highest VAT exemption thresholds in Europe when adjusted for purchasing power. The distribution of Czech corporations shows a sharp spike just below the VAT registration cutoff, and the bunching point has shifted together with increases in the threshold.

Recent threshold increases

Several European countries have recently raised or approved increases to their VAT registration thresholds.

Hungary raised its threshold from HUF 18 million to HUF 20 million in 2026, equivalent to an increase from €45,250 to €50,280. It is scheduled to rise again to HUF 22 million, or €55,310, by 2027.

Poland increased its threshold from PLN 200,000 to PLN 240,000 from 2026, equivalent to an increase from €47,170 to €56,610.

Romania increased its threshold from RON 300,000 to RON 395,000 in September 2025, equivalent to an increase from €59,500 to €78,340.

Belgium’s parliament approved raising the VAT threshold from €25,000 to €30,000 in April 2026, although entry into force is still pending.

Policy implications

VAT thresholds can simplify tax compliance for smaller firms, but high thresholds can also create significant economic costs. They may encourage businesses to stay artificially small, underreport revenue, or avoid productive expansion.

The main policy tradeoff is between reducing compliance burdens for small businesses and limiting distortions that affect business size, competition, and tax revenue.

The article argues that policymakers should reduce these costs by lowering or eliminating VAT exemption thresholds.

Source article: taxfoundation.org