The US federal tax system has changed from a relatively narrow revenue model based mainly on tariffs and excise taxes into a complex progressive income tax system used to fund a much broader range of federal programs. Over 250 years, the tax base, rates, revenue sources, and taxpayer burdens have shifted sharply.

Early federal revenue relied on tariffs and excise taxes

In colonial America, tariffs, also called customs duties, and excise taxes supplied much of government tax revenue. Other taxes, including head taxes, poll taxes, and faculty taxes, also existed, but trade and consumption taxes were central.

This reflected the mercantilist thinking of the period. Governments sought to build wealth and power by maximizing exports, minimizing imports, and taxing specific goods such as alcohol, coffee, and tobacco.

Anger over British taxes imposed without colonial consent helped set the stage for the American Revolution. After independence, the United States continued relying mostly on tariffs and excise taxes.

In 1791, Congress introduced the country’s first internal excise tax on distilled spirits. At that time, the federal government was still small and lacked a broad system for tracking and taxing individual incomes.

The Constitution also limited direct taxation. Article I, Section 8, Clause 1 authorized Congress to “lay and collect” taxes, but direct taxes had to be apportioned among the states. That made a national income tax constitutionally difficult before later changes.

For much of the country’s early history, tariffs and excise taxes remained the main federal revenue sources, even though both were vulnerable to changes in global trade and international conflict.

The Civil War introduced the first federal income tax

The Civil War forced a major change in federal taxation. To raise money for the Union war effort, Congress passed the Revenue Act of 1862, which created the first individual income tax and expanded excise taxes.

That income tax did not last. Congress repealed it in 1872 after the war ended.

A second attempt came with the Wilson-Gorman Tariff Act of 1894, which distinguished between taxing individual income and corporate income. The relevant provisions were later found unconstitutional.

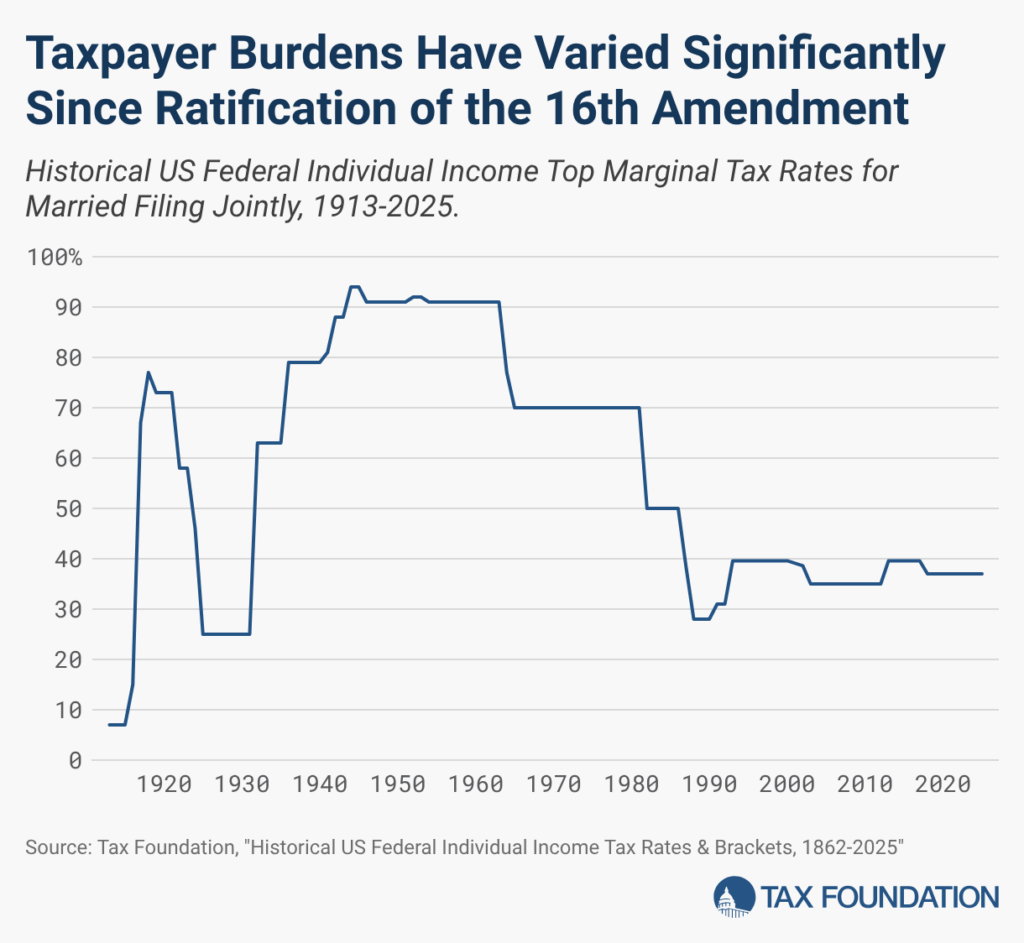

The modern federal income tax arrived only after the 16th Amendment was ratified in 1913. That amendment allowed the federal government to tax income without the earlier apportionment barrier.

The Revenue Act of 1913 reestablished the individual income tax and allowed federal taxes to be levied on both individuals and businesses.

At first, the income tax applied only to high earners, with a top rate of 1%. World War I changed that quickly. By 1918, the top rate had risen to 77%.

Under President Coolidge, later reforms reduced the top rate to 25% by 1925. During the Great Depression and World War II, under President Roosevelt, the income tax expanded substantially, and the top rate reached 94% by 1944.

Since then, the income tax has been the largest source of federal revenue in most years.

The early 20th century added new tax types

The early 20th century also brought several major new taxes:

- Estate tax: introduced in 1916

- Gift tax: introduced in 1924

- Sales tax: introduced in 1930, at the state and local level

- Social Security payroll taxes: introduced in 1937

World War II marked a permanent shift in the scale of federal taxation. Before 1941, the federal government rarely collected more than 5% of GDP in tax revenue, and state and local governments generally raised more revenue than the federal government.

After World War II, federal tax receipts have remained above 15% of GDP in most years, and federal spending has stayed above pre-war levels.

Modern tax reform lowered rates but did not remove complexity

In the decades after World War II, top marginal tax rates remained high, while the tax code became more complex through deductions, exemptions, and special provisions.

President Kennedy’s tax reforms reduced the top income tax rate to 70% by 1965.

Major reforms followed in the 1980s:

- The Economic Recovery Act of 1981 reduced individual tax rates and allowed accelerated depreciation for business investment.

- The Tax Reform Act of 1986 cut rates, flattened the rate structure, and broadened the tax base.

More recent reforms include the Tax Cuts and Jobs Act of 2017, which lowered individual and corporate marginal income tax rates and expanded the standard deduction.

The One Big Beautiful Bill Act of 2025 made much of the 2017 law permanent.

Between those two laws, Congress passed the Inflation Reduction Act, which included energy provisions, a new excise tax on stock buybacks, and a complex alternative minimum tax for large companies.

The long-term pattern

Over 250 years, the US tax system has moved through several stages:

- early reliance on tariffs and excise taxes;

- temporary Civil War income taxation;

- constitutional authorization of the modern income tax in 1913;

- major expansion during the world wars;

- permanent postwar federal revenue levels above earlier norms;

- repeated reform efforts that lowered some rates but left a complex tax code.

The result is a federal tax code that is far more complex and burdensome than the system early American taxpayers experienced. Even after reforms in 2017 and 2025, the structure remains much broader than the original tariff-and-excise model.

Source article: taxfoundation.org