European tax policy debates increasingly focus on competitiveness and economic growth, not only fairness and anti-avoidance. The source argues that Europe’s growth challenge requires better tax design, especially in corporate taxation, rather than focusing only on statutory tax rates or broad EU-level harmonization.

Why Growth Matters for Europe

Economic growth is presented as important not only for individual opportunity but also for governments’ ability to defend their values and interests in a more hostile geopolitical environment.

Europe faces several economic pressures:

- Declining populations

- Rising welfare costs

- Energy security risks

- Growing fiscal demands from defense spending

- Aging populations

- Debt reduction needs

- Climate investment pressures

The European Commission has forecast EU GDP growth of 1.4% in 2026 and 1.5% in 2027. Deficits are expected to rise to 3.4% of EU GDP.

The International Monetary Fund’s forecasts show faster 2026 growth elsewhere:

- North America: 2%

- South America: 2.2%

- Asia and Pacific economies: 4.1%

- Africa: 4.3%

The source argues that these comparisons make stronger European competitiveness more urgent.

Tax Competitiveness Is More Than the Headline Rate

The source argues that tax reform debates too often focus on visible rates, such as the corporate tax rate or VAT rate, while ignoring the broader tax base and how the system works in practice.

Two countries can have the same corporate tax rate but very different rules for:

- Depreciation

- Loss carryforwards

- Selective incentives

- Cross-border tax treatment

- Debt versus equity financing

- Retained versus distributed earnings

- Minimum taxes, surtaxes, or overlapping levies

These design features affect investment incentives, firm location decisions, innovation, productivity, and long-term growth.

To assess tax systems, the source uses the Tax Foundation’s International Tax Competitiveness Index, or ITCI. The index measures tax systems across five pillars:

- Corporate taxes

- Individual income taxes

- Consumption taxes

- Property taxes

- Cross-border tax rules

The ITCI combines tax rates with indicators of tax-base design, neutrality, and simplicity.

The analysis uses data for 23 European and comparable OECD economies from 2014 to 2024 and examines links between changes in tax competitiveness and real GDP per capita growth.

Overall Tax Design Matters

The source finds that countries with more competitive overall tax systems tend to perform better economically.

The main point is that growth-friendly tax policy is not just about choosing one “good” or “bad” tax. It is about whether the full tax system raises revenue efficiently while limiting unnecessary distortions.

A country with moderate rates but a broad, neutral, and predictable tax base may perform better than a country with lower headline rates but a narrow, complex, and distortionary tax code.

The source argues that policymakers should focus first on the overall tax mix, including the combined effect of multiple taxes and rules on households and firms.

Corporate Tax Reform Shows the Clearest Growth Effect

The source argues that broad tax reform is often politically difficult because of coalition politics, fiscal constraints, and administrative limits. In that environment, targeted reforms matter.

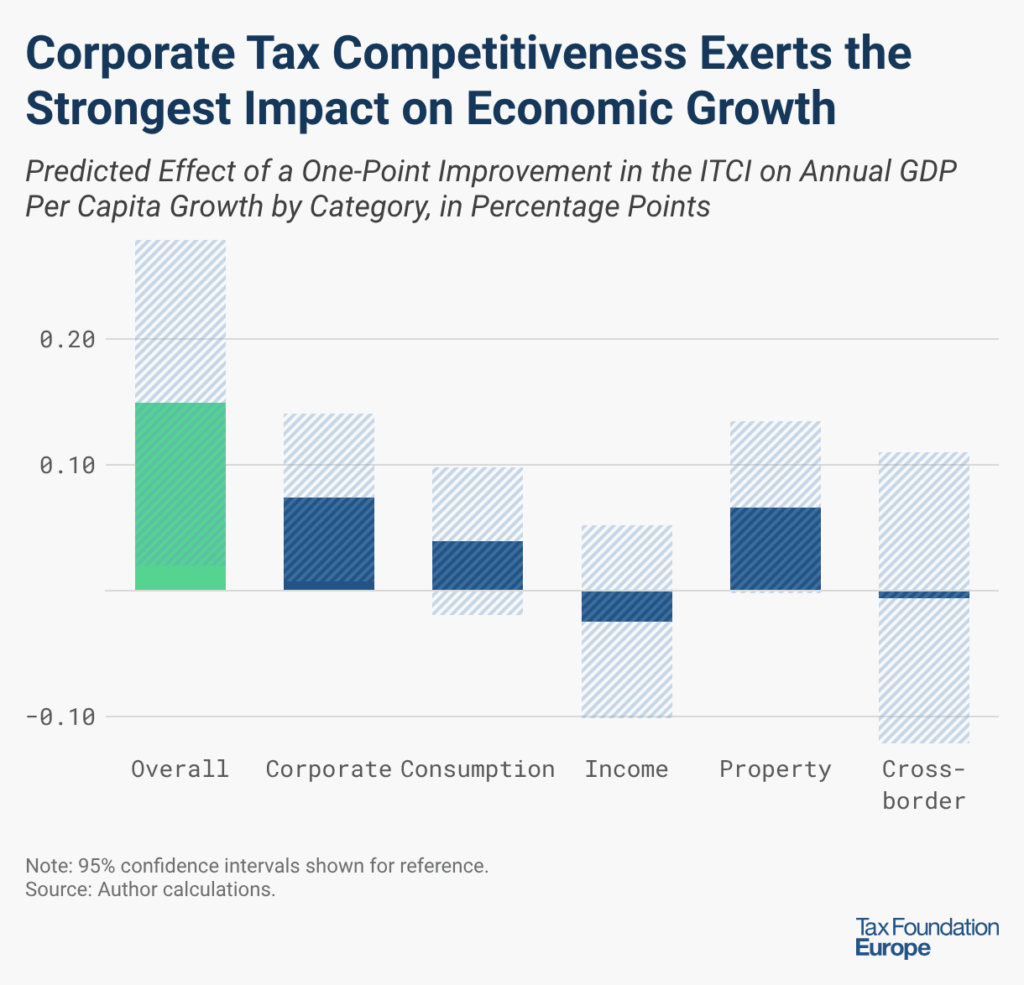

The evidence points most clearly to the corporate tax system.

When the ITCI is broken into its five pillars, the corporate tax component is the only category with a robust and consistent positive association with growth across the main specifications.

The source estimates that:

- A one-point improvement in the corporate tax competitiveness score is associated with about 0.07 percentage points higher annual GDP per capita growth.

- In dynamic estimates, the cumulative effect rises to about 0.16 percentage points over three years.

- A one standard deviation improvement in the corporate category score, equal to 14.3 points, translates into roughly 1 percentage point higher annual GDP per capita growth and 2.29 percentage points over three years.

For 2025, the corporate score ranges from 28.54 points for France to the standardized maximum of 100 points for Latvia.

The source notes that these gains are meaningful in Europe’s low-growth environment, where many advanced economies grow at around 1% to 1.5% annually in real per capita terms.

Why Corporate Tax Design Matters

Corporate taxation directly affects:

- Investment incentives

- Cost of capital

- Financing choices

- Entrepreneurship

- Firm location decisions

- Productivity growth

- Medium-term economic expansion

The source emphasizes that the lesson is not simply “lower corporate tax rates produce growth.” The relevant issue is the competitiveness of the broader corporate tax base.

Important design features include:

- How much investment cost firms can deduct in real terms

- Depreciation, amortization, and expensing rules

- Loss carryforwards and carrybacks

- Debt-equity tax treatment

- Retained versus distributed earnings

- Surtaxes, minimum taxes, and overlapping levies

- Differential treatment for patent income

- R&D tax subsidy design and complexity

The source argues that firms respond to effective tax rates and the broader effective marginal tax burden on investment, not just headline statutory rates.

It also notes that complexity can weaken reform. Many firms fail to claim tax benefits for which they are eligible, especially when compliance is difficult.

What the Evidence Shows

The source draws four main conclusions from the European data.

First, improvements in overall tax competitiveness are linked to stronger growth. Once standard controls are included, the relationship between the aggregate ITCI score and GDP per capita growth becomes statistically significant and remains robust.

Second, the growth effect is not evenly distributed across taxes. The corporate tax pillar is the only component that consistently shows a statistically robust positive relationship with GDP per capita growth.

Other pillars show less consistent effects:

- Consumption tax competitiveness is positive in some models but not consistently significant.

- Individual income tax competitiveness does not show a robust measurable growth effect in the sample period.

- Property taxation is occasionally positive but not consistently significant.

- Cross-border tax rules do not show clear short-run independent effects.

Third, the estimated magnitudes are meaningful. A one standard deviation increase in corporate tax competitiveness is associated with roughly 1 percentage point higher annual GDP per capita growth and 2.29 percentage points over three years.

Fourth, the impact of corporate tax competitiveness builds over time. The effect is positive in the year of reform but becomes larger and more precisely estimated over the medium term, consistent with the time firms need to plan, finance, and implement investment.

EU Harmonization Can Help, But Only If It Improves Tax Design

The source argues that EU tax harmonization can support growth when it reduces cross-border frictions and improves tax systems compared with national rules.

Harmonization may be useful where it reduces:

- Double taxation

- Administrative burdens

- Uncoordinated withholding tax practices

- Cross-border compliance frictions

However, harmonization is not automatically growth-enhancing. The harmonized policy itself must be more economically efficient than the status quo in Member States.

The source criticizes recent EU-level proposals for not focusing enough on growth-friendly tax design.

The 28th Regime and Missing Tax Design

The European Commission has proposed a “28th Regime” intended to make scaling across the Single Market easier for startups by allowing them to operate under a single rule set valid in all Member States.

The source notes that the proposal does not include a tax element.

According to the source, a tax component could have clarified open questions about the taxation of stock options and replicated best practices across the European Union.

The success of such a regime would depend not only on approval by Member States but also on whether businesses gain a real economic benefit from opting into it.

BEFIT and Capital Cost Recovery

The source also discusses the prior BEFIT proposal, which aimed to create a fictitious tax base to simplify screening of cross-border businesses for transfer pricing compliance.

If implemented, BEFIT could have encouraged Member States to align domestic corporate tax bases with the BEFIT base to avoid duplicative compliance costs.

However, the source argues that the proposed BEFIT base neglected key trade-offs in tax design.

An evaluation using Tax Foundation Europe’s European Tax Policy Scorecard found that adopting the harmonized BEFIT proposal would have:

- Improved capital cost recovery in 7 of 27 Member States

- Weakened capital cost recovery in 20 of 27 Member States

Because capital cost recovery directly affects the cost of capital investment, the source presents this as an example of harmonization that may streamline compliance but worsen an important growth-related feature of corporate tax design.

The BEFIT proposal was not adopted.

Lessons From VAT Harmonization

The source notes that European tax policy has improved alongside harmonization in the past.

One example is the replacement of harmful turnover taxes with value-added taxes in early European countries, followed by harmonized VAT legislation at the European level and adoption by new EU Member States.

The source frames this as an example of harmonization that worked because it improved tax systems rather than merely standardizing them.

Policy Direction

The source argues that Europe’s tax challenge is not simply to tax less, but to tax more efficiently.

For national and EU policymakers, the core priorities are:

- Focus on the full tax system, not just headline rates

- Improve corporate tax structures beyond statutory rates

- Support capital formation and investment

- Simplify rules where complexity weakens incentives

- Use harmonization only where it reduces frictions and improves existing systems

- Build on Member State best practices rather than imposing weaker common rules

The central conclusion is that competitive corporate tax policy is an important part of Europe’s growth strategy. In a low-growth environment with rising fiscal and geopolitical pressures, better corporate tax design may offer one of the clearest tax-policy routes to stronger investment, productivity, and long-term economic performance.

Source article: taxfoundation.org